Required Minimum Distributions

What is a Required Minimum Distribution?

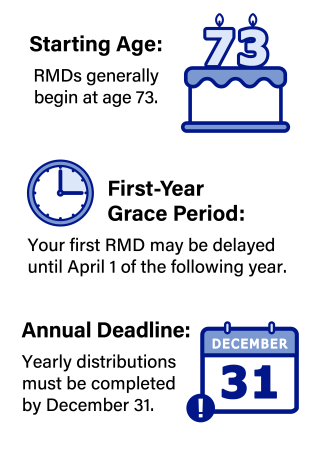

A Required Minimum Distribution (RMD) is the minimum mandatory amount that must be withdrawn each year from retirement accounts, designed to ensure that individuals pay taxes on their tax-deferred savings over time rather than deferring them indefinitely. It applies to traditional IRAs, rollover IRAs, SIMPLE and SEP IRAs, as well as many employer-sponsored plans such as 401(k)s, 403(b)s, and 457(b)s. The withdrawal is mandated by the Internal Revenue Service (IRS) starting at age 73. By requiring withdrawals, the IRS guarantees that retirement funds that have grown tax deferred are distributed gradually and taxed during the account holder’s lifetime.

By when do I have to take the Required Minimum Distribution?

As required by the Internal Revenue Service, PRCUALife must notify IRA account holders who are required to take a Required Minimum Distribution for the tax year. You must generally take your RMD by December 31 each year. However, your first RMD can be delayed until April 1 of the year following the year you turn 73—this is known as your required beginning date under rules set by the IRS. If you choose to delay your first RMD until April 1, you will need to take two distributions in that following year: one by April 1 (for the prior year) and another by December 31 (for the current year). After your first distribution, all subsequent RMDs must be taken by December 31 each year.

Is the Required Minimum Distribution taxable?

Yes, an RMD is generally taxable. Because traditional IRA contributions are made on a tax-deferred basis, withdrawals are typically taxed as ordinary income and must be reported to the IRS. After the end of the year in which you take the distribution, you will receive a tax form detailing the total amount withdrawn and the taxable portion to help you prepare your income tax return. Large withdrawals can push you into a higher tax bracket or increase your Medicare premiums.

What if I don’t take my Required Minimum Distribution on time?

If you do not take your RMD by the deadline, or if you withdraw less than the required amount, you may be subject to a penalty from the IRS. The penalty is 25% of the amount that should have been withdrawn, in addition to owing regular income tax on the distribution. This can be reduced to 10% if the mistake is corrected within two years. If you don’t need the money, you can use a Qualified Charitable Distribution (QCD) directly from your IRA to a charity tax-free, which satisfies your RMD.

Can I roll over the Required Minimum Distribution?

No, an RMD cannot be rolled over to another tax-deferred retirement account. The IRS does not allow RMD amounts to be reinvested into a qualified retirement plan or IRA for continued tax deferral. However, after you receive the distribution, you may choose to invest those funds in a non-qualified account—such as an existing or new annuity— with PRCUALife, or another trustee, to allow future earnings to grow on a tax-deferred basis, subject to the rules of that account.

Can I withdraw more than my Required Minimum Distribution?

Yes, you can withdraw more than your Required Minimum Distribution each year. However, any amount you take above your required minimum will not count toward or reduce your RMD for future years, as required under rules established by the Internal Revenue Service.

How do I calculate my Required Minimum Distribution amount?

Your RMD is not a fixed number; it changes every year based on your account balance as of December 31 of the previous year; your Life Expectancy Factor, a divisor found in IRS Publication 590-B (most use the Uniform Lifetime Table); and a set formula consisting of your prior year-end balance divided by the Life Expectancy Factor. Your RMD amount is calculated using IRS life expectancy tables, based on either single or joint life expectancy, depending on your election.

If you own multiple IRAs, an RMD must be calculated separately for each account. However, you may withdraw the total combined RMD amount from one IRA or from multiple IRAs, whether held with PRCUALife or another financial institution. Because IRA distributions are generally taxable, we strongly encourage you to consult your tax advisor or attorney before making decisions. You may also refer to IRS Publication 590-B for additional guidance.

Please refer to these Uniform Life Expectancy Tables and Examples to help you understand how your RMD is calculated. To ensure your RMD is processed on time, complete and return Distribution Request Form before your RMD deadline. If you have questions about your RMD or need assistance completing the form, please contact our Member Services Department—we are happy to help.

How do I start taking my Required Minimum Distribution?

Once you have read the information on this page and are ready to begin taking your required minimum distribution, please complete the Distribution Request Form electronically or mail all pages of the form to us at:

Annuity Processing

PRCUALife

984 N Milwaukee Ave

Chicago, IL 60642-4101

How can I contact PRCUALife if I have additional questions about my RMD?

The PRCUALife Member Services Department is available Monday-Friday, 8 a.m. to 5 p.m., to answer any questions you may have. Please call (773) 782-2753 or email info@prcua.org.